Small, medium or large ASBL: which category does yours actually belong to?

Law of 7 August 2023: FTEs, income, assets — the three criteria for classifying your ASBL as small, medium or large. A 10-minute diagnosis.

📅 Last verified: 24 May 2026. This article applies Article 18 of the law of 7 August 2023, which sets out the categorisation of ASBLs. The law of 4 December 2024 amended other articles (day-to-day management, updating of articles of association), but not Article 18.

The essentials in 30 seconds

- The law of 7 August 2023 classifies every ASBL into three sizes — small, medium, large — according to three criteria: full-time equivalent (FTE) employees, annual income and total balance sheet assets.

- You are a small ASBL as long as you do not exceed at least two of the following three thresholds: 3 employees, €50,000 in income, €100,000 in assets. This is the case for the vast majority of Luxembourg associations.

- You only move up into the higher category once the thresholds have been exceeded over two consecutive financial years — the new regime then applies to the following year.

- Your category determines your accounting obligations: simplified accounting (small), double-entry (medium), double-entry plus an audit by an approved chartered auditor (large).

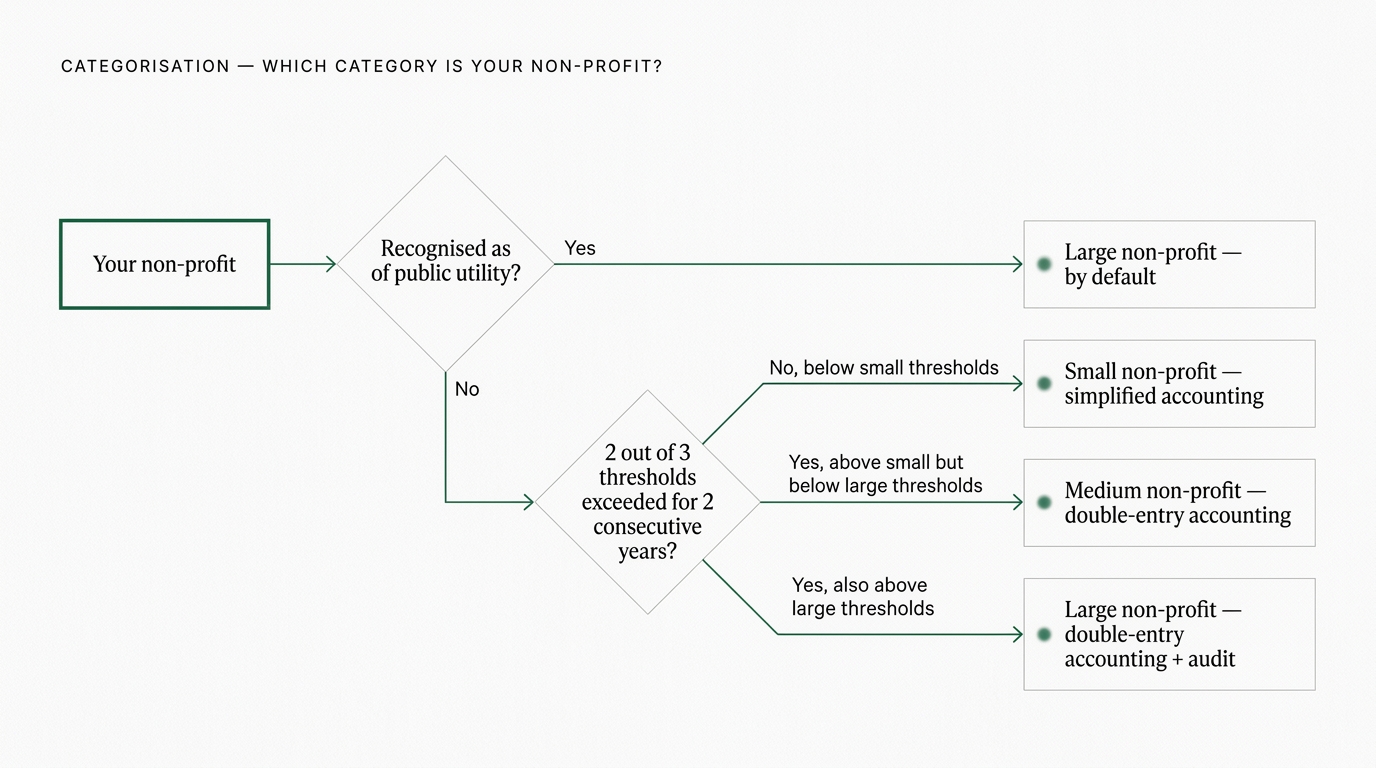

- ASBLs recognised as of public utility fall under the accounting regime applicable to large ASBLs (full accounting plus audit), regardless of their actual size; foundations follow an equivalent regime.

📥 Want the answer in 2 minutes?

The Veräin interactive diagnosis asks you 4 questions, identifies your category and sends you a PDF checklist in your association's name.

Why this categorisation, and why now?

Before 2023, all Luxembourg ASBLs were subject to the same rules, whether they employed fifty staff or kept their cash in a paper notebook. The law of 7 August 2023 introduces a logic of proportionality: the larger an association, the higher the accounting requirements. A village brass band and a large employer-ASBL no longer play in the same regulatory league — and that is good news for small structures.

The categorisation is therefore not a pointless administrative exercise. It directly governs the accounting you must keep, what you must file with the Trade and Companies Register (RCS), and whether your accounts must be audited by an approved professional. Classifying yourself correctly is the starting point for any compliance work.

If you are not yet familiar with the general framework of the law, start with our reference article: The law of 7 August 2023 explained simply. This guide focuses on a single question, but takes it to the end: which category are you in, concretely?

The three criteria, explained one by one

Article 18 of the law sets out three numerical criteria. Here are the thresholds that separate the categories:

| Criterion | Small ASBL | Medium ASBL | Large ASBL |

|---|---|---|---|

| Employees (FTE) | fewer than 3 | 3 to 15 | more than 15 |

| Annual income | up to €50,000 | €50,000 to €1,000,000 | more than €1,000,000 |

| Total assets | up to €100,000 | €100,000 to €3,000,000 | more than €3,000,000 |

📌 How to read this table. The law does not define the "medium" category by a standalone bracket. It sets two tests: you are small as long as you do not exceed at least two of the three lower thresholds (3 employees, €50,000, €100,000), and large as soon as you do exceed at least two of the three upper thresholds (15 employees, €1,000,000, €3,000,000); the medium category is everything in between. The thresholds are inclusive: reaching exactly €50,000 in income does not "exceed" the threshold. It is this mechanism — detailed in the diagnosis below — that is authoritative, not the columns of the table. These amounts may also be amended by Grand-Ducal regulation: check the version in force.

Let's look at each criterion closely, because it is in the calculation details that mistakes tend to hide.

1. Full-time equivalent (FTE) employees

The law refers to the "number of staff members employed full-time and on average during the financial year" (Article 18). In other words, it does not count heads but working time brought back to a full-time basis — what is commonly called the full-time equivalent (FTE).

- A full-time employee = 1 FTE.

- A half-time employee (50%) = 0.5 FTE.

- Two employees at 50% = 1 FTE in total.

In practice, an ASBL employing one full-time coordinator and two half-time activity leaders counts as 2 FTE — it remains below the 3-employee threshold on this criterion.

💡 Calculation method: the law does not specify in detail how this average is to be calculated (a Grand-Ducal regulation may clarify it). In practice, employees' working time is brought back to a full-time basis, averaged over the financial year.

⚠️ What does not count as staff: the criterion refers to employees bound by an employment contract. Volunteers, even if they receive an expense allowance or a stipend, are not employees and therefore do not enter the calculation. Likewise, external service providers invoicing fees (an independent accountant, for example) are not your employees.

2. Annual income

This criterion aggregates everything the ASBL takes in during the financial year in connection with its activity:

- membership fees,

- donations and gifts received,

- public grants received,

- activity income (ticketing, bar, sales, services),

- miscellaneous income linked to operations.

The idea is to measure the actual economic volume of the association over a year. One point of vigilance: certain flows do not reflect genuine economic activity — internal recharges, transfers between accounts, reversals of accounting provisions. Exactly how to handle these flows depends on your accounting system and, in case of doubt, deserves the advice of your accountant.

⚠️ Multi-year grants: if you receive in a single payment a grant intended to cover several years, the way it is treated (allocated to a single financial year or spread out) may momentarily push your income above a threshold. This is precisely the kind of situation where the "two consecutive financial years" mechanism (see below) protects you from a premature change of category.

3. Total balance sheet assets

Total assets means everything the ASBL owns at the closing date of the financial year:

- cash (bank accounts, petty cash),

- receivables (sums owed to you, grants to be received),

- tangible fixed assets (equipment, vehicles, real estate),

- financial fixed assets (investments, deposits).

💡 Don't have a formal balance sheet? This is the case for many small ASBLs on simplified accounting. In that case, make a pragmatic estimate: add up the balance of your bank accounts and petty cash on the closing date, plus the value of your durable equipment, plus the sums owed to you. In the vast majority of cases, a small ASBL is very far from the €100,000 asset threshold — you will see it immediately.

The diagnosis in 3 questions

Ask yourself the three questions, in this order. The chart below leads you to your category.

The key rule fits in one sentence: you check whether you exceed at least two of the three thresholds of a category. Exceeding a single criterion is not enough to change your size.

⏳ The two-financial-year rule — Exceeding the thresholds does not change your category immediately. You must have exceeded (or fallen back below) at least two of the three thresholds over two consecutive financial years. The new regime only applies afterwards, in the financial year following those two years of crossing. This delay is deliberate: it gives you time to adapt your accounting before the new obligations apply.

📥 Is your case unusual?

Seasonal staff, shifted financial year, public-utility status… The interactive diagnosis covers these situations and returns your category along with the checklist of obligations that follow from it.

Special cases

Most ASBLs fall clearly into one category. But a few situations deserve careful reading.

ASBLs recognised as of public utility

An ASBL recognised as of public utility must, regardless of its actual size, keep full accounting under the regime applicable to companies and have its accounts audited by an approved chartered auditor — that is, the level of requirements applicable to large ASBLs (Article 28). Even with a single employee and a €20,000 budget, this is the regime that applies. It must also submit its accounts and budget to the Ministry of Justice each year within the month of their approval. This is the counterpart of the benefits attached to public-utility status.

Foundations

Foundations are not ASBLs, but the law subjects them to an accounting regime equivalent to that of large ASBLs (Article 53): double-entry accounting, annual accounts prepared under the regime applicable to companies, retention of records for ten years, and audit of the accounts by an approved chartered auditor or an accountant. Like public-utility ASBLs, they submit their accounts and budget to the Ministry of Justice. Size-based categorisation therefore does not apply to them — they fall straight into the most extensive regime.

ASBLs employing seasonal or short-term staff

If you employ seasonal staff (sports coaches over a season, summer activity leaders) or short fixed-term contracts, the question is: how do you count them in the FTEs? The FTE principle is based on actual working time brought back to an annual full-time basis. A coach employed at 30% over the year counts as 0.3 FTE; a seasonal employee present for a few weeks weighs an even smaller fraction. In practice, a volunteer-led sports association with a few part-time coaches almost always remains well below the 3-FTE threshold. In the event of a complex payroll structure, have your calculation validated by your social secretariat.

ASBLs with a shifted or mid-year-changed financial year

If you change the closing date of your financial year (for example to move from a calendar year to one aligned with the sports season), the transition year may be shorter or longer than twelve months. Your income and FTEs for this atypical year must be read with that distortion in mind: an 18-month financial year mechanically inflates cumulative income. Here again, the two-consecutive-financial-years rule cushions one-off effects.

Groups of ASBLs and consolidation

Where a "network head" ASBL coordinates legally distinct entities, each ASBL is in principle assessed on its own figures, unless there is a specific consolidation requirement. The structures concerned by potential consolidation are rare and already supported by an accounting professional; if that is your case, it is a question to address with them.

What your category actually changes

Once classified, here is what applies to you. It is this table that makes the diagnosis useful.

| Obligation | Small ASBL | Medium ASBL | Large ASBL |

|---|---|---|---|

| Accounting | Simplified: statement of receipts and expenses + notes | Double-entry: balance sheet + profit-and-loss account + notes | Double-entry, full accounts under the regime applicable to companies |

| Audit | No mandatory external audit | No mandatory auditor | Audit by an approved chartered auditor |

| RCS filing | Yes — simplified statement | Yes — annual accounts | Yes — full annual accounts |

| Filing deadline | 7 months after closing (approval at 6 months + filing within the month) | Same | Same |

| Record retention | 10 years | 10 years | 10 years |

Three important remarks:

- All categories file with the RCS. This is one of the major novelties of the law: even a small ASBL must file a simplified statement of its accounts, within seven months of the end of the financial year. The details of this filing are the subject of a dedicated upcoming article: ASBL annual accounts: step-by-step preparation and RCS filing.

- The shift to double-entry accounting is the heaviest change to anticipate for an ASBL that is growing. If you are approaching the thresholds of the medium category, this is the moment to consider a proper accounting software rather than a simple spreadsheet.

- The audit by an approved chartered auditor (large ASBLs and public-utility ASBLs) is a cost and lead-time item to factor into your annual calendar.

What to do once you've classified yourself

You know your category. Here are the three concrete moves that follow, depending on your size.

If you are a small ASBL (the most common case):

- Keep a rigorous receipts-and-expenses register: date, amount, nature, supporting document filed.

- Note in your calendar the RCS filing deadline: seven months after your closing date.

- Check that your articles of association and your RBE registration are up to date — that is often where the real work lies, not in the accounts.

If you are a medium ASBL:

- Move to double-entry accounting if you haven't already, with software adapted to the Standard Chart of Accounts (PCN 2020).

- Prepare a balance sheet, profit-and-loss account and notes for the next closing.

- Anticipate the filing of the full accounts with the RCS within the deadlines.

If you are a large ASBL (or a public-utility ASBL):

- Contact an approved chartered auditor early enough in the year: their diaries fill up, and the audit conditions your filing.

- Structure your accounting to produce full annual accounts.

- If you are of public utility, don't forget the annual activity report to be sent to the Ministry of Justice.

💡 Unsure about your category or your obligations? The Veräin interactive diagnosis does the calculation for you and sends you a personalised checklist in your association's name — ideal to present at your next general meeting.

📥 Classify your ASBL in 5 minutes and receive your personalised checklist — free interactive diagnosis. For the full framework of the law, (re)read our reference guide on the law of 7 August 2023.

Frequently asked questions

Q: We exceed only one of the three thresholds. Do we change category? A: No. You must exceed at least two of the three thresholds to fall under the higher category — and have done so over two consecutive financial years. Exceeding a single criterion (for example a one-off spike in income) is not enough.

Q: Do volunteers receiving an expense allowance count as FTE employees? A: No. Only employees bound by an employment contract enter the FTE calculation. A volunteer receiving an expense allowance or a stipend remains a volunteer, not an employee.

Q: We received a large one-off grant that pushes us above an income threshold. Do we have to change our accounting from next year? A: Not immediately. The two-consecutive-financial-years rule is designed for this: a one-off overshoot in a single year does not trigger a change of category. It is only after two financial years above the thresholds that the switch happens, and only from the third financial year onwards.

Q: Our ASBL has no balance sheet. How do we assess total assets? A: Make a pragmatic estimate: balance of bank accounts and petty cash at closing, plus the value of your durable equipment, plus receivables. A small ASBL is almost always very far from the €100,000 threshold.

Q: Our ASBL is recognised as of public utility but remains small. Which regime applies to us? A: The regime for large ASBLs, regardless of your actual size: double-entry accounting and audit of the accounts. This is the counterpart of public-utility status.

Q: Where do I find the reference text? A: It all rests on Article 18 of the law of 7 August 2023. The law of 4 December 2024 amended other articles of the law (day-to-day management, updating of articles of association), but not Article 18 on categorisation.

Going further

This article is part of our series on the law of 7 August 2023. To go deeper:

- The law of 7 August 2023 explained simply — the reference guide (pillar article)

- ASBL articles of association not compliant with the 2023 law: 5 clauses to check (upcoming)

- ASBL annual accounts: step-by-step preparation and RCS filing (upcoming)

- Administrative dissolution without liquidation: is your ASBL at risk? (upcoming)

📬 Want to receive the next article directly by email? Subscribe to the Veräin Media newsletter — one in-depth article per month, never spam, unsubscribe in one click.

This article was written by Veräin Media, which offers independent content on the management of Luxembourg ASBLs. It does not constitute legal advice and is not a substitute for consultation with a lawyer or accountant for specific situations. If you spot an error or want to report a regulatory development, contact us at contact@veraein.lu.

Main sources: Law of 7 August 2023, Article 18 (Legilux) — Law of 4 December 2024 (Legilux) — Ministry of Justice: ASBL information page. Last verified: 24 May 2026.

Follow

Follow Veräin Media to never miss an upcoming publication and join the conversation.