The 7 August 2023 law explained simply: what changes for your non-profit in Luxembourg

Everything the new Luxembourg non-profit law changes for your association: categorisation, accounting obligations, RCS filing, sanctions. A clear, up-to-date guide.

📅 Last verified: 23 May 2026. This article reflects the law of 4 December 2024, which amended several articles of the original law.

The essentials in 30 seconds

- The law of 7 August 2023 replaces the 1928 law and modernises the entire body of law governing Luxembourg non-profits (ASBLs) and foundations.

- It introduces a three-tier categorisation of non-profits (small, medium, large) with proportional accounting obligations.

- Annual accounts must now be filed with the RCS within seven months of the end of the financial year.

- The board of directors may meet by videoconference and pass circular resolutions — modernity enters non-profit law.

- A non-profit that has filed nothing with the RCS for five years and does not respond to reminders risks administrative dissolution without liquidation.

- The 24-month transition period ended on 23 September 2025: all non-profits are now subject to the new law, even those that have not updated their bylaws.

Introduction

Nearly a century. That is how long the law of 21 April 1928 lasted, governing Luxembourg's non-profit associations and foundations until 22 September 2023. A law suited to its era — the era of municipal music societies, village brass bands and hunting clubs — but largely outdated for a non-profit sector that today counts more than 8,281 ASBLs and 219 foundations, employer of hundreds of thousands of volunteers and several thousand staff.

The law of 7 August 2023 marks a break. It does not merely refresh the 1928 law: it rewrites the entire Luxembourg non-profit law. Accounting, governance, financial transparency, dissolution, merger, donations — every aspect of the operation of a non-profit is reworked, sometimes deeply.

This modernisation arrives in a largely volunteer-run sector, historically organised in an artisanal manner, where the finances often rest on a few people who do everything. For many non-profits, the new law is not just a change of rules: it is a call to professionalise a bit more, without losing the associative spirit that defines them.

This article takes stock. Without unnecessary jargon, getting to the point for volunteers who need to understand what changes, and with enough precision for experienced treasurers and fiduciaries to find what they need.

Why this new law?

Three main reasons led the Luxembourg legislator to overhaul non-profit law:

1. A text that had become anachronistic. The 1928 law was designed neither for videoconferences nor for email convocations, nor for non-profits employing dozens of staff. It also ignored the modern governance tools of commercial companies, which many structured non-profits now draw inspiration from.

2. Growing European pressure. Obligations arising from EU law — particularly in the field of anti-money-laundering and counter-terrorism financing — required a more demanding and transparent framework. The creation of the Register of Beneficial Owners (RBE) in 2019 had prepared the ground; it was necessary to go further on accounting transparency and governance.

3. A demand from the sector itself. Non-profit federations, fiduciaries and the most structured non-profits had long been calling for reform: to clarify grey areas (what is a member? an honorary member?), to authorise modern practices (videoconference, electronic signatures) and to make obligations proportional to the actual size of the structures.

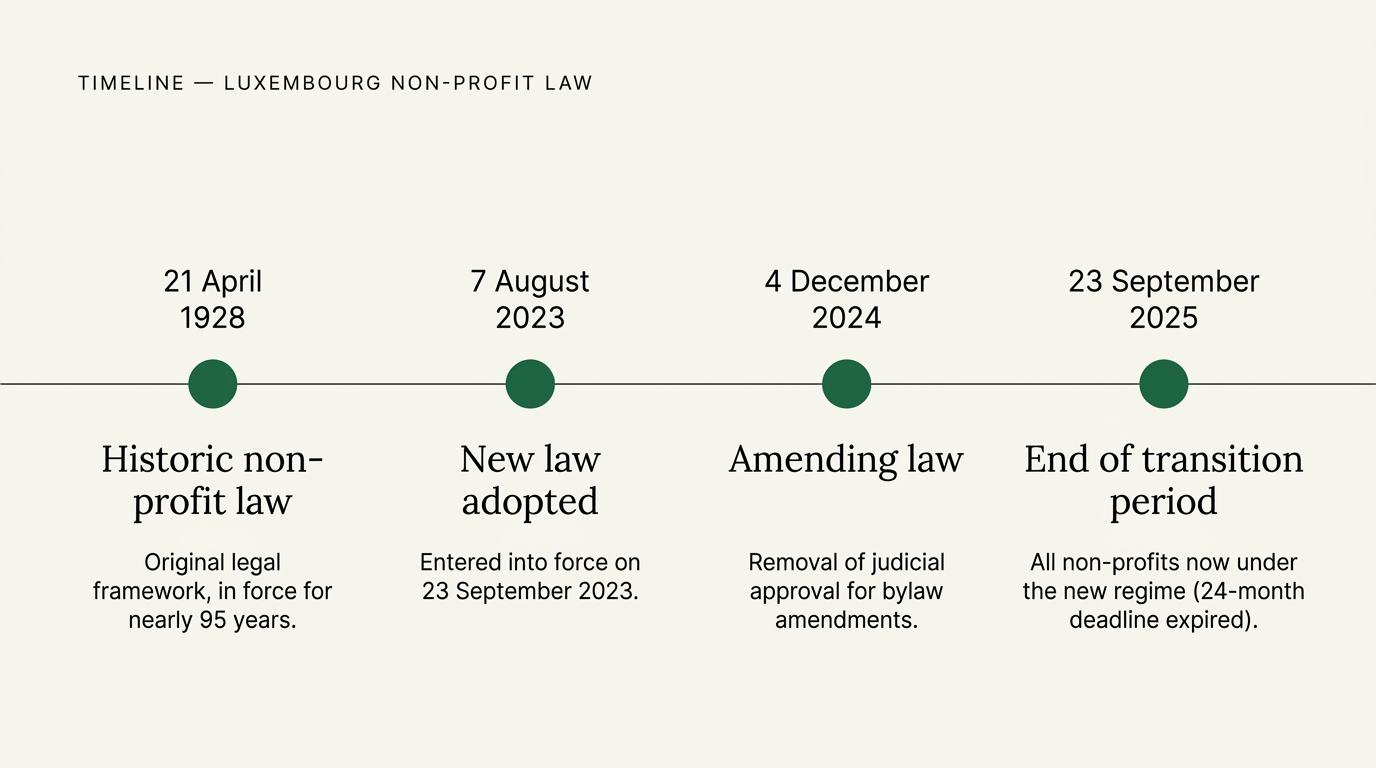

The law of 7 August 2023 responds to these three pressures. It was adopted by the Chamber of Deputies on 28 June 2023, published in the Official Journal on 19 September 2023, and entered into force on 23 September 2023.

📚 Going further — The law of 4 December 2024 clarified two points: it completely removed the judicial approval procedure for bylaw amendments (which was required in certain cases previously), and clarified the rules on delegation of day-to-day management. These adjustments further simplify the administrative procedures.

A four-point chronology

The nine key changes that transform the life of non-profits

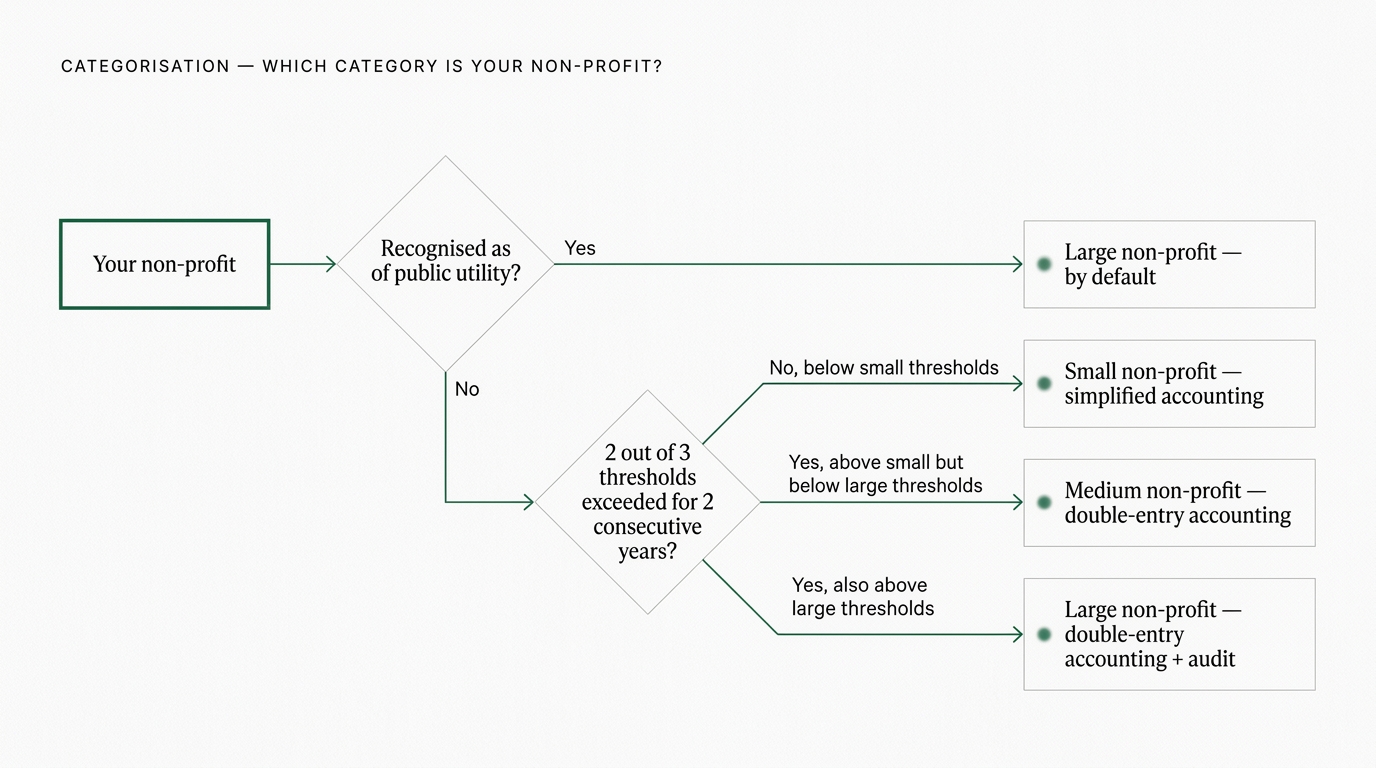

1. Categorisation of non-profits by size

This is probably the most structural change. The law introduces three categories of non-profits, based on three numerical criteria:

- Number of full-time equivalent employees

- Total annual income

- Total assets on the balance sheet

A non-profit belongs to a category as long as it does not exceed, over two consecutive financial years, at least two of the three thresholds of the higher category. The change of category takes effect from the third financial year.

The thresholds (Article 18 of the law):

| Criterion | Small non-profit | Medium non-profit | Large non-profit |

|---|---|---|---|

| Employees (FTE) | < 3 | 3 to 15 | > 15 |

| Annual income | ≤ €50,000 | €50,000 to €1,000,000 | > €1,000,000 |

| Total assets | ≤ €100,000 | €100,000 to €3,000,000 | > €3,000,000 |

This categorisation directly determines the accounting obligations (see change no. 2) and certain governance requirements.

Note: Non-profits recognised as of public utility are automatically treated as large non-profits, regardless of their actual size. Foundations are subject to the regime applicable to large non-profits in accounting terms.

2. New accounting obligations, proportional to size

A simple logic guides the new accounting obligations: the larger the non-profit, the higher the expected rigour.

- Small non-profits: simplified accounting. It is enough to keep a register of receipts and expenses, like a rigorous cash book. No balance sheet, no formal profit-and-loss account.

- Medium non-profits: double-entry accounting, with balance sheet, profit-and-loss account and notes. Application of the Luxembourg Standard Chart of Accounts (PCN 2020). Abbreviated format permitted.

- Large non-profits: double-entry accounting and obligation to have the accounts audited by an approved chartered auditor. This is the gradual alignment with the standards of mid-sized commercial companies.

For public-utility non-profits, regardless of size: they are subject to the regime for large non-profits and must additionally submit an annual detailed activity report to the Ministry of Justice.

Accounting documents and their supporting documents must be retained for ten years after the end of the relevant financial year.

3. Mandatory filing of annual accounts with the RCS

This is a major novelty for many non-profits. Article 18 of the law provides that:

- The board approves the accounts within six months of the end of the financial year.

- The accounts are then filed with the Trade and Companies Register within the month following this approval.

- They are published in the Electronic Compendium of Companies and Associations (RESA) within a total period of seven months post-closing.

For a non-profit closing its financial year on 31 December, this means: approval by the AGM no later than 30 June of the following year, filing with the RCS in the following month, publication in the RESA no later than 31 July.

This obligation applies to all categories of non-profits subject to the new law — including small ones. The form of the filing differs however: small non-profits file a simplified statement, medium and large ones file their complete accounts.

4. Remote meetings and circular resolutions

The law formally enshrines two modern practices that the 1928 law did not explicitly provide for:

- Videoconferencing is now possible for both board meetings and general assemblies, provided that the technical means allow identification of participants and effective participation with continuous broadcasting. Unless the bylaws provide otherwise, directors or members who participate are deemed present for the calculation of quorum and majority.

- Circular resolutions (decisions taken without a physical meeting, by written exchange) are authorised for the board only in exceptional cases duly justified by urgency, provided they are taken unanimously and the bylaws expressly authorise them. It is therefore not a routine method of operation — the normal route remains the meeting (physical or videoconference).

Convocations to the board and the AGM can also be sent electronically — without recourse to traditional registered mail. The law directly authorises this method (by post or electronically), without specific bylaw conditions.

For non-profits whose directors are geographically dispersed (national sectoral associations, federations, non-profits with volunteers abroad), it is a change that really simplifies daily life.

5. Simplification of the member register

Under the old law, non-profits had to file annually with the civil court registry the modifications of the list of their members. It was an administrative obligation that weighed especially on small structures and brought little value.

The 2023 law radically simplifies: the member register simply needs to be kept up to date at the seat of the non-profit, in paper or electronic format. No more annual update filing with the RCS.

In return, rigour in maintaining the register is expected: every member, every director and every supervisory authority must be able to access it on simple request. For a large non-profit or a public-utility non-profit, it is a document to be kept with seriousness.

6. The threshold for donations raised to €30,000

To receive an inter-vivos gift or testamentary bequest above a certain amount, a non-profit had to obtain ministerial authorisation. The threshold has been raised to €30,000 by the new law.

Better still: a new exception has been introduced. If the donation takes the form of a bank transfer from a credit institution authorised in an EU or EEA Member State, no authorisation is required, regardless of the amount.

Concretely, this means that a significant donation made by SEPA transfer from a Luxembourg, French or German account can be accepted immediately by a non-profit, without administrative procedures. A real simplification for non-profits that mobilise private funding.

For donations above €30,000 that do not go through EU/EEA transfer (inheritances, gifts in kind, donations from outside the EU), the authorisation procedure by ministerial decree remains applicable (Article 19 of the law).

7. Administrative dissolution without liquidation

This is a new procedure, aimed at cleaning up the register by eliminating non-profits that have ceased all real activity without proceeding with their formal dissolution.

The mechanism is simple: if a non-profit has made no filing with the RCS for five years and does not respond within six months to the update request from the RCS manager, it can be administratively dissolved without liquidation.

This procedure is a pragmatic response to a real problem: many non-profits created 20 or 30 years ago have no more activity, sometimes no more identifiable members, but still exist legally and pollute the official registers.

For an active non-profit, the risk is zero as long as it regularly files its accounts and updates. For a dormant or poorly tracked non-profit, the risk is real.

8. Restructuring tools: transformation, merger

The new law finally makes available to non-profits restructuring tools inspired by commercial company law:

- A non-profit can now transform itself into a foundation or into a societal impact company without losing its legal personality (and therefore without having to liquidate its assets and create a new one).

- Two or more non-profits can merge by absorption (one absorbs the other) or by establishment of a new non-profit resulting from the union of the two.

These mechanisms are mainly of interest to structured non-profits, federations seeking to rationalise their landscape, or associations in difficulty wishing to attach themselves to a more solid structure.

For a classic small non-profit, these tools will probably never be mobilised. But their existence is a signal: the law brings non-profit law closer to the tools available to companies.

9. Bylaw update: formal obligation, limited sanction

Article 77, paragraph 1 of the law imposes a formal obligation: every non-profit established before 23 September 2023 was required to bring its bylaws into harmony with the provisions of the new law within a 24-month period — a deadline that expired on 23 September 2025. The Ministry of Justice qualifies this harmonisation as a "legal obligation".

In practice, the direct sanction in case of inaction is limited: no fine is provided for the mere fact of not having adapted the bylaws. Statutory clauses contrary to the new law are simply deemed unwritten (Article 77, paragraph 4) — they cease to have effect, and the mandatory provisions of the law apply in their place. Only an extreme case — operation of the non-profit rendered impossible — can lead a district court to pronounce dissolution at the request of any interested party.

Three practical reasons to proceed with the update without delay:

- Secure daily operation — if your bylaws contain provisions contrary to the new law (quorum rules, board composition, mode of convocation), the law prevails. You risk operating out of step with your own statutory framework, which can generate internal disputes in case of a contested vote or decision.

- Fully activate modern provisions — for videoconferencing (board and AGM), the bylaws may specify the modalities; for circular resolutions in case of urgency, express statutory authorisation is required. An up-to-date set of bylaws avoids any ambiguity.

- Prepare future developments — modern, compliant and complete bylaws are also the foundation of good governance for the future: merger, transformation into a foundation, hiring of staff, opening to complex financing.

Good news: since the law of 4 December 2024, the update is purely administrative. Decision at the AGM according to your existing quorum rules, then filing of the updated version with the RCS. No more judicial approval to request.

Which category of non-profit do you belong to?

Before going further, it is useful to make the diagnosis on your own association. The category determines all your future accounting and reporting obligations.

Three questions to ask yourself:

- How many employees do you employ in full-time equivalents (as of the closing date of the last financial year)?

- What is your total annual income (membership fees, donations, subsidies, miscellaneous receipts)?

- What is your total balance sheet assets (or, in the absence of a balance sheet, the estimated value of your assets: cash, equipment, real estate)?

The diagnosis:

An important nuance: it is only from the third consecutive financial year in which you exceed the thresholds that you officially change category. This leaves time to adapt to the new accounting obligations that accompany the change.

The transition period: ended on 23 September 2025

To allow existing non-profits to adapt, the law provided for a 24-month transition period from its entry into force on 23 September 2023. During this period, non-profits established before this date had two options:

- Quickly adapt their bylaws to switch to the regime of the new law (and immediately benefit from its modern provisions: video, circular resolutions, etc.).

- Keep their original bylaws during the transition period and remain subject to the 1928 law until expiry.

This transition period ended on 23 September 2025. Since this date, all non-profits without exception are subject to the law of 7 August 2023, even those that have not updated their bylaws.

⚠️ An important consequence: if your bylaws contain provisions contrary to the new law (for example, rules on quorum, majority, or board composition that are no longer compliant), the provisions of the law prevail, not your bylaws.

Sanctions in case of non-compliance

The new law is more demanding than that of 1928 in terms of transparency and respect for reporting obligations. Four types of risks may materialise, from the most direct to the most diffuse:

| Type of breach | Sanction incurred | Range / Consequence | Competent authority |

|---|---|---|---|

| Failure to register, delay or inaccuracy in RBE | Criminal fine | €1,250 to €1,250,000 | Public prosecutor, on investigation by judicial police |

| Inactivity with RCS for 5 years + no response within 6 months to reminder | Administrative dissolution without liquidation | Legal disappearance of the non-profit | RCS manager |

| Non-filing of annual accounts with RCS within 7 months | Civil liability of directors in case of harm to a third party | Variable depending on harm | Civil courts, on action by harmed third party |

| Financial opacity or non-transparent accounts | Reputational risk | Loss or suspension of grants, withdrawal of partners | Public and private grantors |

What to do now?

Many Luxembourg non-profits have functioned for years with light tools: shared spreadsheets, paper folders, oral transmission between successive treasurers. This system has held up, sometimes very well — it is part of the artisanal identity of the sector. The new law does not condemn it, but it demands an additional notch of rigour from all non-profits on three fronts: bylaws, accounting, traceability.

The goal is not to overturn your operation overnight. It is to identify the few actions to take, in the right order, to bring the non-profit up to standard without overload.

Here is an actionable checklist, prioritised:

This week:

- Identify your category (small, medium, large) according to the three criteria seen above.

- Check your bylaws: do they date from before September 2023? Do they contain explicit provisions on videoconferencing, circular resolutions, mode of convocation? If not, plan their update.

This month:

- Check your RBE registration (Register of Beneficial Owners). If it has not been updated following a change of board, do it immediately.

- Confirm the date of your financial year and calculate your next RCS filing deadlines (six months for approval + one month for filing = seven months post-closing).

In the next three months:

- Prepare the update of your bylaws: circulate a draft to directors, plan a dedicated extraordinary AGM if necessary.

- Update your accounting practices according to your category: transition to double-entry for medium ones, contact with an approved chartered auditor for large ones.

In the next six months:

- Audit your member register: up to date, accessible, compliant with the new law?

- Document your compliance: an internal file that groups together your updated bylaws, the RBE certificate, the filed annual accounts, the minutes of the last AGM. It is the reflex that protects the non-profit and its directors.

Frequently asked questions

Q: Our non-profit is very small (a neighbourhood brass band, no employees, €2,000 of membership fees per year). Are we really concerned? A: Yes, but with lighter obligations. You are a small non-profit, you can keep simplified accounting (receipts and expenses), and your filing obligations remain minimal. The main point of attention: make sure your bylaws comply with the new law, and that your RBE registration is up to date.

Q: Our bylaws have never been updated since 1995. Are we illegal? A: Your non-profit exists legally. The law (Article 77, paragraph 1) formally required bringing the bylaws into harmony with the new provisions within a 24-month period after its entry into force — therefore before 23 September 2025 — and the Ministry of Justice qualifies this harmonisation as a "legal obligation". Since this date, however, no fine is provided for the mere fact of not having adapted your bylaws: statutory clauses contrary to the new law are simply deemed unwritten (Article 77, paragraph 4). The update remains strongly recommended to clarify your operation, ideally at your next general assembly.

Q: Must we hold a mandatory annual AGM? A: Yes, the new law maintains the obligation of an annual general assembly, which must in particular approve the annual accounts within six months of the end of the financial year. This AGM can now be held by videoconference if your bylaws allow it.

Q: For foundations, what changes? A: Foundations fall under an accounting regime close to that of large non-profits (double-entry accounting, annual accounts under the regime for companies, enriched notes, retention of records for 10 years). The audit of annual accounts can be entrusted to an approved chartered auditor or an accountant at the choice of the board. Like any Luxembourg legal entity registered with the RCS, foundations remain subject to the declaration obligation with the Register of Beneficial Owners (RBE) — the founder and members of the board are declared there. On governance, the modernised principles (board videoconferencing, written resolutions in case of urgency by unanimity) also apply.

Going further

This article is the first in a series dedicated to the new law on non-profits and foundations. The next articles will go step by step into each of the key topics.

📬 Want to receive the next article directly by email? Subscribe to the Veräin Media newsletter — one in-depth article per month, never spam, unsubscribe in one click.

This article was written by Veräin Media, which offers independent content on the management of Luxembourg non-profits. It does not constitute legal advice and is not a substitute for consultation with a lawyer or accountant for specific situations. If you spot an error or want to report a regulatory development, contact us at contact@veraein.lu.

Main sources: Law of 7 August 2023 (Legilux) — Ministry of Justice: new non-profit law. Last verified: 23 May 2026.

Follow

Follow Veräin Media to never miss an upcoming publication and join the conversation.